Category: Investment Blog

Where Are You Going, Where Have You Been?

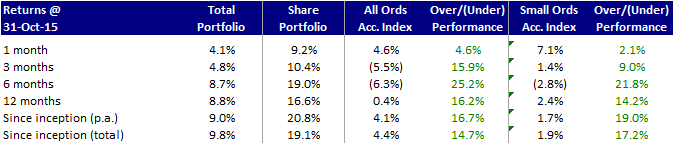

I haven’t written here for what seems like an eternity. The good news is that unlike many people that start a similar blog and then stop because they are performing badly, my portfolio has continued to perform reasonably well. I’ll put up a more detailed performance update soon but the portfolio is up overall and continued to outperform the two comparison indices, although the gains have slowed over the past few months.

The main reason that I took some time out was because I’ve been doing a large amount of research and reading. Since I’m not a full-time investor and have a young family and busy job, it was either the research or the writing and writing took a back seat this time. The main reason I chose a period of research over the writing is the ongoing level of central bank monetary accommodation and extraordinary stimulus programs globally and making sure that I have a better grasp of how this is influencing the markets and what may happen as the various monetary stimulus programs start to unwind. This took me on a pretty winding journey covering topics such as the implementation of the various quantitative easing programs, the fractional reserve banking system, how credit is created in today’s banking system, the various components of the monetary supply, Austrian economics, the gold standard and many more related topics. Amongst all that, I even managed to fit in a reasonable amount of other general reading on investing and behavioural economics.

This was an incredibly interesting period and even though I have a background in finance and banking, I learned a huge amount. I think that many people without a background in finance would be truly amazed at how the banking system functions, the relationship between central and commercial banks and some of the implications of monetary debasement. I’ll pick up on various topics as we move forward but there are two that are worth mentioning now.

Firstly, most of what I uncovered was pretty scary in terms of possible effects on stock markets globally – I was already somewhat worried which is why I am only half invested in the market – and so the question becomes what to do. As I’ve stated previously, I don’t believe in market timing for macro factors. You may get lucky once or twice and hit the top/bottom or hit a major macro event, but all the evidence (both research and anecdotal) suggest that it is almost impossible to do so consistently. Therefore, I don’t want to reduce my exposure any further. I don’t want to short the market because it could continue to go well north of where it is today – in fact often in bull markets the biggest gains come right toward the end. I also don’t have the personal constitution/I’ve settled on a mix of actions:

- I’m periodically purchasing out of the money ASX 200 index puts. This gives you downside protection in a similar way short selling, but unlike shorts you can only lose your initial investment so can control your exposure. In this way, it’s very similar to an insurance policy (i.e., small outlays over time that could result in a big payoff if the market tanks). In addition, I also believe that the pricing is reasonably favourable currently due to suppressed volatility (one of the key inputs to options pricing).

- I have some of my portfolio invested in gold. I fully agree with people that say gold is not a productive asset and I am not including it to serve that purpose (or for short term speculation for that matter). It is being included purely as insurance for (i) general protection from uncertainty (i.e., performs well in down markets), and (ii) also as a hedge against a total meltdown of the current monetary system, which could result in reverting to gold-backed currencies (not as far-fetched as it may seem) – if this occurs I believe that gold could appreciate significantly from it’s current price.

- Ongoing vigilance of the debt levels of companies in my portfolio and companies that I am evaluating. This is a liquidity driven credit market and if that liquidity dries up, I believe that there will be significant dislocation (tightening) of the credit markets, so I want companies with low levels of debt – this was already a strong focus for me, but I’ve stepped up my scrutiny in this regard.

Note that I won’t include either of the put positions and gold purchases (regardless of whether they perform well or not) in the returns analysis on this website as I consider them to be insurance/hedging policies that are separate from my ‘long-only’ investing.

The second thing that I want to note here relates to central bank influence. It is generally accepted that the capitalist system of free markets with open price discovery and signaling (through prices) has generated the fastest growth in living standards, productivity, economic output etc. In particular capitalism has proved to be effective at allocating scarce resources to meet society’s needs. Society’s needs are conveyed through prices – if there is high demand prices go up and encourage further supply and vice versa. Once you lose the informational content contained in prices (e.g. in many communist societies where prices are set centrally), these links break down and resources are not allocated nearly as effectively in terms of meeting society’s needs.

What has been interesting over the past few years in particular is to see many (most) developed capitalist societies start relying on a central banks setting interest rates. Interest rates are simply a price, and so we find ourselves in a position where the price for the most important commodity in existence (money itself) is being set centrally and has lost all signaling value. How far we are from ‘natural’ interest rates is very hard to guess because it is not easily observable unless the market for money ((i.e., interactions between private-sector lenders and borrowers) are functioning freely.

I have no doubt that the central bankers manipulating interest rates through monetary policy genuinely believe that they are doing the right thing. However, it has been shown over and over again throughout history that a few people making decisions generally do a very poor job compared to hundreds of thousands of people interacting through an open market. Some of the results of this are somewhat puzzling. For example, as the debt burden has gone up globally interest rates have been falling rather than rising. This is due to people having the belief that central bankers know what they are doing and will be able to successfully pull off what would be an enourmous balancing act of stimulating the global economy without their monetary policies causing massive price inflation. If people ever lose their faith that the central bankers will be able to accomplish this, then those central bankers will no longer be able to dictate interest rates – rather, the market will tell them that their borrowing cost are actually much higher than the rates that they have been setting, and the whole thing falls apart.

Without getting into big predictions as to whether or when this will happen, I will (for now) simply make the comment that monetary accommodation on the scale that is currently occurring and in so many developed countries/regions at once has never been seen before. At the very least, we need to recognize that this adds a large amount of macro risk (not to mention many of the other effects that artificially low interest rates have) and to try and make sure that we have a plan should it break the wrong way.

Portfolio Performance (Month 21)

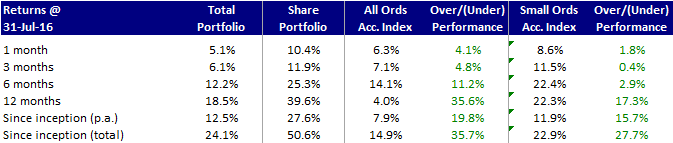

Over the 3 months to 31 July 2016 my share portfolio continued to outperform the benchmark indices, returning 11.9% for the 3 month period compared to 7.1% for the All Ordinaries Accumulation Index and 11.5% for the Small Ordinaries Accumulation Index.

The best performers during the period were:

- MACA Limited (MLD), up 57% over the 3 months on limited news;

- Boom Logistics (BOL), up 39% over the 3 months on the back of a succesful refinancing of its debt facilities – the company now has more flexibility in terms of its debt amortisation profile and one can only hope that management uses this additional flexibility to send cash back to shareholders, preferably through a share buyback, rather than easing off the cost cutting and asset sales (the aggressive amortisation under the previous debt facility actually ensured that management applied disipline in relation to those items);

- Gale Pacific (GAP), up 30% for the period based on positive updated earnings guidance;

- BSA Limited (BSA), also up 30% primarily due to a large contract win for work relating to the nbn; and

- Jumbo Interactive (JIN), which was up 27% for the three months, again based on positive earnings guidance – the value of the Australian database/business is starting to shine through as the negative performance in Germany is minimised.

The only really poor performer during the period was Brierty Limited (BYL), which was down 34%. However, the stock has already lost so much that a 34% move actually doesn’t mean that much from a $ perspective. I mentioned in a previous post that it is increasingly looking like the company was being mismanaged rather than just a downtrodden mining services company. Forager Funds recently shared similar thoughts. As with Forager, Brierty Limited is just part of a basket of mining-related stocks that I bought when things were looking particularly bleak for the sector. Over the whole basket, I have a positive return and still see significant upside in some of my positions. In some ways this confirms the basket approach to this sort of situation – however, it is still frustrating to have the courage to go against the grain, be generally proved right about the identification of significant value on offer (at least to date), but have some of that value destroyed by poor management of one of the companies in the basket.

Due to some trimming of profitable positions, I am now less than half invested, with the balance in cash. I would like to get back to at least half of my portfolio being invested, but haven’t found anything particularly attractive on offer over the past few months. Coming out of full year earnings reporting season I will actively be looking for opportunities to invest some of my cash balance. This often produces opportunities for value investors due to over-reaction or under-reaction to what is reported.

Portfolio Performance (Month 18)

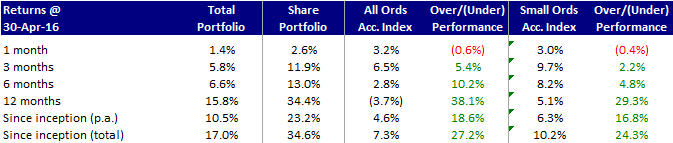

Over the 3 months to 30 April 2016 my share portfolio has continued to outperform the benchmark indices, returning 11.9% for the 3 month period compared to 6.5% for the All Ordinaries Accumulation Index and 9.7% for the Small Ordinaries Accumulation Index.

Some of the better performers during the period were:

- INTECQ (ITQ), up 74% over the 3 months on the back of strong interim results (net profit before tax up 83%) and some contract wins for its gaming services and technology – there appears to be plenty of runway for continued growth in the future;

- Codan (CDA), up 67% over the 3 months driven by contract wins and a very strong business performance update (net profit after tax expected to be up 57% for FY16 compared to FY15);

- Service Stream (SSM), up 62% for the period primarily due to contract wins, a capital return announcement and solid first half results; and

- MACA Limited (MLD), which was up 57% for the three months.

The main drags on the portfolio return during the period were:

- Brierty Limited (BYL), down 32% over the three months and definitely under review as its looking more and more like a poorly managed company rather than just a downtrodden mining services company;

- Reckon (RKN), down 26% for the period and a stock which I have now sold out of and discussed at length here; and

- Watpac (WTP), down 23%, but which I feel has been unfairly caught up in the mining services sector pummeling despite most of its business coming from building construction (where it continues to win new projects) rather than mining services.

I continue to be approximately half invested in cash.

March 2016 Buys and Sells (Part 1)

I generally do not trade very often. However, with the half-year earnings season, it ended up being a relatively busy March for me. Below is an outline of my selling activity. My buys will follow at a later date.

Complete Exits

Collins Foods (CKF)

- Gain/Loss: 107%

- IRR: 93%

- Rationale: Sold out at $5.10 which I thought was approaching a fair value for the stock. Since then the stock traded back down to around $4.00 and I considered buying back in, but I wanted the price to fall further before doing so and the stock has subsequently traded back up to around $4.20. I still like the business itself due to its steady (profitable) expansion through new stores and refurbishment of existing stores, as well as the fact that there are further margin improvements likely to come from the KFC restaurants it acquired in WA (which had a lower operating margins than the rest of their KFC restaurants). I also suspect that the stock would exhibit reasonably good defensive characteristics in an economic downturn – think the McDonald’s effect where many customers swap more expensive casual restaurants for their cheaper fast-food offering when times are hard. If you think, as I do, that we may be on the brink of a global recession, then this stock may be worth considering. I’ll continue to monitor this one.

Pacific Brands (PBG)

- Gain/Loss: 97%

- IRR: 232%

- Rationale: Also sold out due to my view that the stock was approaching fair value. See my detailed post here.

Reckon (RKN)

- Gain/Loss: -8%

- IRR: -7%

- Rationale: This investment was based on a simple thesis for me. The company is a provider of software solutions primarily for do-it-yourself accounting aimed at small to medium-sized businesses, small office/home office users and personal wealth management sectors in Australia and New Zealand and competes with Xero and MYOB. The business had been showing consistent growth in revenues, EBITDA and net income over a long period of time and seemed to be adapting well to making its products more available via the cloud – however, it was still trading at a pretty favorable valuation on a number of fundamental metrics such as P/E ratio or EV/EBITDA. The only reason that I could conclude for this was that the growth rates hadn’t been as high as the market might have liked.

What I believed that the market may be missing was firstly that the company had made a big push towards a subscription based service rather than one-off upfront purchases of the software. This increases the recurring nature of the revenue making it far more stable over time. Therefore, whilst the growth hadn’t been spectacular, the quality of the earnings had improved markedly over time. In addition, the nature of the product makes it incredibly ‘sticky’. Once small businesses make the initial choice of accounting software, there is a large cost (both financial and time investment) to change to an alternative software provider, which provides these types of businesses with a form of a moat through large barriers to exit. My belief that the market wasn’t giving the company full value for these factors, as well as the favorable fundamental valuation criteria were the basis of (and thesis for) my investment.

Towards the end of 2015, there was much speculation that potential acquirers were looking at the business. Indeed the company even hired a financial adviser, which is generally uncommon unless they suspected that someone may put in a takeover offer. The speculation and news that they had hired an adviser drove the price up towards $2.50 at the end of 2015 and I was showing nice paper gains from my $1.80 entry price.

Then came the 2015 full year results. The company announced that they had undertaken a strategic review and were going to undertake a number of new initiatives including making a significant push into new markets in the United States and United Kingdom and accelerating development spend on new products. In addition they also announced an acquisition of an online document management company in the United States. All of these items were going to result in significant investment over the next few years which changed the nature of the company from a steady, defensive investment to a more aggressive growth focus which was not in line with my original investment thesis.

This investment is going to have significant impacts on financial performance over the next few years. You can already see the impact of this for the 2015 financial year in the bridge that was provided by the company in the results presentation. Absent the investment, the company’s steady growth rate was maintained. However, EBITDA actually declined with the investment taken into account.

The effect is going to be even more pronounced next year (and I suspect for a further couple of years after that).

Ultimately, this expansion into the United States and United Kingdom and accelerated investment into their products may pay off very handsomely. However, I think that there is a lot more risk to this new strategy than growing organically (albeit more slowly) in the Australian and New Zealand markets. As such, I decided to exit the investment. Unfortunately, the market also wasn’t excited about the changes and I ended up taking a bit of a loss overall, although the damage was minimal. This will be an interesting one to keep an eye on in the future. If their expansion strategy is showing signs of failing, the price could fall much further and the value of the Australian and New Zealand business could be masked (assuming that it continues to improve slowly over time). This could give rise to an opportunity for value investors.

STW Communications Group (SGN)

- Gain/Loss: 44%

- IRR: 83%

- Rationale: Clearly someone else saw the value that I saw, because within 6 months of my purchase a merger was announced with WPP’s Australian and New Zealand businesses. Although it was announced as a ‘merger’, it was really a friendly takeover by WPP who was already a large shareholder in STW Communications and now holds over 60% of the stock post merger. The transaction was unusual in that WPP contributed its Australian and New Zealand businesses at an agreed value and took shares in return at an issue price of $0.915 (based on that agreed value) which was a 30% premium to the trading price before announcement. After the announcement, the stock traded around $1.00 for a while and I ended up selling out at $0.98. In my mind, additional value from here depends upon the successful integration of the businesses and achievement of significant synergies. This will not be a simple task as there are a large amount of businesses involved and probably multiple back-office systems that need to be reconciled. Both STW Communications’ and WPP’s businesses had been showing declining EBIT leading into the transaction and, when coupled with the costs to achieve the synergies, the near term results may not be great. If management can blend the businesses smoothly and realize the cost and revenue synergies then there is clearly still additional value available. As of today, the market appears to think that management will be successful as the stock is trading at $1.13. However, I feel that I can find other opportunities that have greater upside without the operational risk entailed in achieving synergies in a complex marriage of many different businesses.

Partial Sell-Downs

Macmahon Holdings (MAH)

- Sold 15% of my holding at 12.5 cents per share (my average entry price is 7.7 cents) simply to reduce portfolio weighting which had grown to over 15% as the stock gained value. I still have confidence that there is significant value available at current prices and hope that the company resumes its on market share buyback.

Service Stream (SSM)

- Partial sale based on my automatic selling rule that if a stock is up by two-thirds (66%) I will automatically sell around a third of my holding.

Book Notes – The Education of a Value Investor

I just finished Guy Spier’s book The Education of a Value Investor. Whilst I thoroughly enjoyed the book and would certainly recommend it to people who have read a large amount of books on value investing, it probably won’t go on the recommended reading list on this blog as I’m trying to limit it to a few of my absolute favorite books with really actionable ideas. The most interesting aspect of the book for me was the extent to which Guy took actions in order to tray and avoid the pitfalls of human emotions in his investing. Trying to avoid our inherent psychological and emotional biases is a fundamental part of my approach to investing, so I particularly enjoyed hearing how Guy dealt with the issue. Some of the actions he took included:

- Not just moving office, not just moving cities, but moving to an entirely different country (from the US to Switzerland);

- Removing the Bloomberg terminal from his immediate office space;

- Checking stock prices at most once a week, and only checking the price of one stock at a time;

- Placing orders with his brokers only when the market was closed;

- 2 year moratorium on selling stocks that had fallen significantly in price; and

- Only discussing specific stocks with investors in his fund once he has sold them.

These are just a few of the actions he took, so you can see how concerned he is with the prospect of being influenced by his emotions. One of the things that is helpful when making an honest assessment of this issue is understanding that many of the influences are happening subconsciously. We all like to think that we are slightly different and we will be able to deal with circumstances or information more rationally than other people, which will allow us to avoid psychological biases. However, the reality is that the vast majority of the problem is happening without us even realizing it. Therefore, the best way to deal with the issue is to remove or avoid as many of the circumstances, people and information that may result in our subconscious psyche being affected in a negative way, rather than relying on our ability to rationalize those negative items and ignore them.

Pacific Brands (PBG) – Takeover Offer

Pacific Brands (PBG) recently announced that it received a takeover offer from US company HanesBrands, which the Board has unanimously recommended. Unfortunately, I had fully exited my position in March so didn’t benefit from the premium to the share price. However, I feel that the stock was pretty close to a fair valuation when I sold out so I’m not looking back (with the benefit of hindsight) and regretting my decision. In fact, at the time of selling down I did consider whether a takeover offer might be forthcoming, but my general view is that I shouldn’t buy or hold stocks if the investment result is dependent on a takeover offer as they are notoriously hard to predict.

Here was the history of my trading in Pacific Brands:

- 22 July 2015 – initiated position at $0.46

- 8 December 2015 – sold down a third of my holding at $0.74 based on an automatic selling rule that I have instituted whereby I sell down a third of my holding when it is up by 66% from my original acquisition price unless it is still significantly undervalued and I am overwhelmingly confident of my analysis

- 2 March 2016 – sold down a further third of my holding at $0.95

- 23 March 2016 – sold down the remainder of my holding at $1.01

As mentioned above, I felt that $1.00 per share was close to fair value for the stock, and before the takeover offer the stock actually traded back down to $0.87 per share. The takeover offer was made at $1.15 per share which equated to an EV/EBITDA multiple of 13.5x (based on historical EBITDA pre significant items). I believe that it would have been hard for the stock to trade up to that sort of level in the absence of a takeover.

In the end, this was an extremely successful investment for me, close to doubling my money in 8 months. The key to the success of this investment, was being able to look through a number of non cash impairments to understand what the underlying performance of the business would look like after divesting the Brand Collective unit. In my view, the performance of that unit was significantly masking very strong performance by both Bonds and Sheridan which were Pacific Brands’ two main brands. In the end, the investment thesis played out exactly as I had hoped, but over a much shorter time period than I initially would have imagined (no complaints from me on that).

Reverse Corp (REF) – Value Trap?

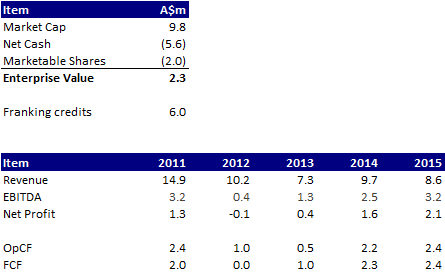

I’m going to start my review of my portfolio’s reporting season with the most disappointing half-year report, which was frustrating for reasons wholly unrelated to the underlying performance of the business. Reverse Corp (REF) is primarily a provider of reverse charge calling services in Australia, allowing users to make calls from out-of-credit pre-paid mobile phones and on all major Australian mobile provider networks and payphones. The company also owns an online contact lens store, OzContacts.com.au, and has at various times in the past had interests in other business lines that have now been exited.

The online contacts business is just break even on an EBITDA basis and not showing particularly fast growth, so I will assume it has no value for the purposes of this analysis. The reverse charge calling services on the other hand is a steady producer of cash flow for the business and has been for some time, allowing the company to build up a significant cash balance (as well as franking credits). The current trading value and recent operating performance of the company is as follows:

As you can see the free cash flow for each of the last two years individually is more than the current enterprise value of the company. However, as can also be seen, the business is in structural decline and this is readily admitted by management and the Board:

While your Board remains committed to the company’s core reverse charge and payphone products, it acknowledges that both areas of operation are under considerable threat from structural industry change. These changes, triggered by the very rapid, global uptake of smartphones, are causing both fixed and mobile telecommunication operators in all markets to radically rethink their business models. The impacts are likely to be profound for the market for reverse charge and payphone services in the long term, but the Board remains confident that the company can continue to operate profitably in these markets in the medium term.

Chairman, 2012 Annual Report

Recognising this, the company started taking steps in FY2012 to exit unprofitable businesses, shut down its international operations and cut costs to manage the profitable Australian businesses for cash. This was exactly the right move and the positive results can be seen in FY2013-2015 as both operating and free cash flow improved significantly. The results were slightly down for the first half of FY2016 (as you would expect), but the business is likely to continue to produce $1-2 million in operating cash flow for at least the next few years.

For a buyer entering at the current valuation, if the cash balance and operating cash flow was returned to shareholders they would likely receive back their initial investment within 1-2 years, and that’s ignoring the substantial value of the franking credits held by the company. However, this is where we start running into the potential value trap issues. Rather than returning the substantial cash balance and ongoing operating cash flows, management decided to invest $2 million in a small minority stake in another listed entity, Onthehouse Holdings (OTH). Quite apart from the business they invested in, which I think is very expensive for what you get (notwithstanding the takeover offer that was forthcoming after the stake was acquired), I am not investing in the company to have management act as a fund manager on my behalf. If I want to take small minority stakes in listed businesses, I can do so myself.

On the face of it, management’s actions appear to be a classic example of the inherent conflict of interest between a management team and the owners of the business. The owners of a business want to see the cash. This is particularly true for dying businesses where the focus should be on maximizing the shrinking cash flow. However, the management team wants to continue getting a salary and will try to revive the dying business or take what cash is available and invest it in other opportunities.

In a best case scenario, the takeover offer that was forthcoming for Onthehouse Holdings after the company purchased its stake will lead to management achieving a profit that can be returned to shareholders. However, it’s a very realistic possibility that the takeover further emboldens them to invest the cash within the business elsewhere. There are not many management teams that can consistently perform M&A well. In fact it is generally a huge destroyer of value for most businesses. All I can say is that if the company makes one more investment similar to Onthehouse Holdings, I’ll be voting with my feet and selling my stock despite the apparent value on offer.

Portfolio Performance (Month 15)

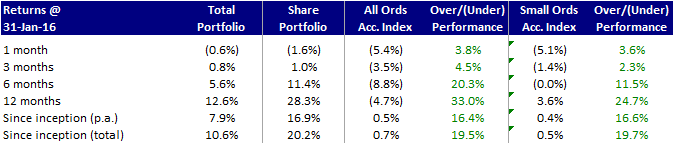

Over the 3 months to 31 January 2016 my share portfolio has continued to outperform the benchmark indices, returning 1.0% for the 3 month period compared to -3.5% for the All Ordinaries Accumulation Index and -1.4% for the Small Ordinaries Accumulation Index. Broadly speaking, the mining-related stocks in my portfolio (e.g., mining services companies) underperformed, while the general industrial companies outperformed. My mining-related stocks had performed very strongly for the 6-9 months leading up to this 3 month period, but were marked down by the market in the face of continued declines in commodity prices in late 2015 and early 2016. I still believe that there is significant value in the basket of mining-related stocks that I hold and so I have generally been happy to hold or add to these positions over time. Note that I don’t hold any pure mining stocks because (i) I don’t know much about mining operations, and (ii) I don’t want that level of straight commodity exposure in my portfolio.

Some of the better performers during the period were:

- Collins Foods (CKF), up 47% over the 3 months, which reported good results on the back of improving margins and a full year of contributions from their (very good) acquisition of a portfolio of KFC restaurants – the market finally seems to be understanding that the poorly performing Sizzler restaurants are not a big driver of the financial performance of the business;

- Pental (PTL), up 36% over the 3 months, which rose after some analyst buy recommendations and positive research reports; and

- Service Stream (SSM) and Thinksmart (TSM) were new additions during the period that both performed strongly.

I have made a number of portfolio changes after the completion of the Australian half-year reporting season and will post some updates on new and exited positions over the upcoming weeks.

Portfolio Performance (Month 12)

One year in and I’ve already had one period of underperformance and one larger period of outperformance. I was significantly underperforming the two benchmark indices (All Ordinaries Accumulation Index and the Small Ordinaries Accumulation Index) up until early 2015 to the tune of over 10%. I should say upfront that I don’t think that either of the indices are particularly great benchmarks for the likely composition of my portfolio. With my particular style of value investing, I expect to hold a fairly heavy weighting of small to medium cap industrial companies and am unlikely to have much exposure to financial, mining, infrastructure or utility stocks. The top 6 stocks in the All Ordinaries Index are composed of the big four banks, Telstra and BHP and these stocks are huge proportion of the overall index. Given this mismatch, it is clearly not a perfect yardstick for measuring my performance. The Small Ordinaries Index is a bit better by virtue of excluding the 100 largest companies and including the next 200 largest companies, but it is still not that great a measure due to the proliferation of mining and energy stocks. However, I firmly believe that long-only funds should always be measured against some index (compared to long/short funds which should have an absolute return target) and these are two of the most freely available index series that take dividends into account.

When looking at performance numbers it is also important to understand what is included or excluded. The numbers presented above are on the following basis:

- Transaction costs (brokerage) are included

- Dividends are included

- Franking credits are not included

- Taxes are not included

I believe that this treatment is consistent with the methodology of the two accumulation indices that I am using as benchmarks (with the exception of the transaction fees which don’t get factored in for the indices, but which should be included in my performance analysis).

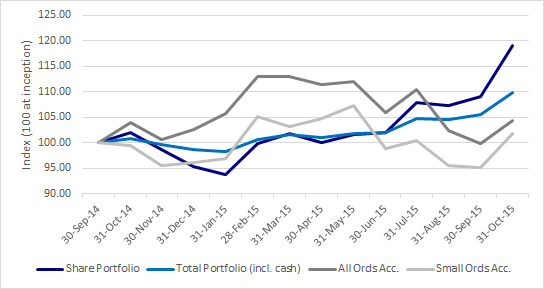

Given the composition of the All Ordinaries Index, it is no surprise that it performed very strongly over late 2014 and early 2015. Sentiment was good and investors in those environments gravitate towards well-known names. The August 2015 market correction had not yet taken place and commodity prices, although clearly on the decline, weren’t nearly as low as they are currently. In contrast, my portfolio over that period of time was on its way down, led almost entirely by poor performance from a basket of mining services and mining-related stocks (I bought them while they were still on the way down) which was partly offset by decent results in the rest of my portfolio.

From early 2015 to the end of October 2015, my portfolio benefited from much better trading results from the mining services and mining-related basket (hopefully they have hit the bottom) as well as a continuation of the good performance of the rest of my portfolio. The banks and commodity players struggled during this time, which significantly impacted the performance of both indices, but in particular the All Ordinaries Accumulation Index. Overall for the first year, I significantly outperformed the benchmarks, with almost all of the outperformance in the second half of this period. Given that it was only a one year period, I wouldn’t read too much into it. I will judge myself over much longer periods of time, but I would be lying if I said that it didn’t feel good to be ahead of the benchmarks after one year.

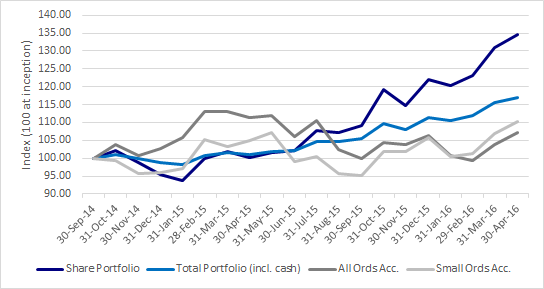

One other thing that you may notice is that I have presented two sets of numbers for my portfolio. One is solely the portion of my portfolio allocated to stocks, and one is the total portfolio including cash holdings. For various reasons that I will discuss in a later post, I am only about 50% invested in stocks at the moment with the remainder invested in cash. As this is a decision that I have consciously made, I feel that it is important to show the overall returns for the whole portfolio including my cash holdings as these are ultimately the returns that I have to live with. However, I also wanted to measure the performance of my stock portfolio separately as that should be compared to the benchmarks. Over time, I intend to be fully invested at which point I will likely only show the overall portfolio including cash, but until that time comes I will continue to show both sets of numbers.

What’s in a name?

My introduction to value investing occurred only about 18 months ago. The catalyst for this was my return to Australia from a long stint overseas and reviewing the performance of my superannuation portfolio which I had entrusted to a major Australian investment house. The performance of the portfolio was very poor and the management fees I was paying them to have the portfolio ‘actively’ managed were pretty large leading to a 20% loss in the 6 years that I was away. Having worked in the financial sector my whole career, I should have known better and I’m sure I’ll post further thoughts on the investment industry and the misalignment of incentives in the future. Anyway, it was at that point that I decided to start taking control of my own portfolio and investment decisions.

I started in much the same way as I imagine many other value investors got hooked, which is by reading “The Intelligent Investor” by Ben Graham. Heralded by Warren Buffett as “the best book about investing ever written”, I figured it was a good place to start – if it’s good enough for Buffet, then it’s plenty good enough for me. I was amazed at how much the book resonated with me. I came to the immediate recognition that what I thought had been people ‘investing’ in the market was mostly pure speculation. For those that haven’t read it, what is truly striking is that despite the original version being written over 60 years ago, the principles explained in it are still so incredibly relevant today. In fact, the way that I look at individual stocks, the market, industry participants and the way that they behave has become so much clearer.

Since then, I have read extensively about value investing and I’m constantly amazed by the variety of approaches and applications of the value investing philosophy. However, from my perspective there tend to be two main tenets of successful value investing:

- Valuation analysis based on some form of fundamental and observable valuation criteria; and

- A highly disciplined approach that ignores or minimizes many of the psychological/emotional pitfalls experienced by most investors.

The more that I read on the topic, the more I become convinced that the second element plays a larger role than most people realise. Through various deep-seated psychological biases, we are inherently flawed in a way that makes it hard to invest in an independent and unprejudiced way. If you look at any of the best value investing books, you will see that this is a common theme.

It’s on this basis that I chose the name of the blog. Admittedly it’s a little dramatic – however, I wanted to choose something that I thought was relevant to the way that I want to invest. Vor is the Viking goddess of discipline and this is the primary goal that I want to try to achieve in my investing. To have the discipline to not let emotion and other psychological biases impede rational thought. To stick with what has been proven to work over the long term. To identify and ignore the hype of industry participants whose incentives are not aligned with mine. To avoid the comfort of following the herd. This will undoubtedly be a hard path – one which will be my own investing Odyssey.