Reverse Corp (REF) – Value Trap?

I’m going to start my review of my portfolio’s reporting season with the most disappointing half-year report, which was frustrating for reasons wholly unrelated to the underlying performance of the business. Reverse Corp (REF) is primarily a provider of reverse charge calling services in Australia, allowing users to make calls from out-of-credit pre-paid mobile phones and on all major Australian mobile provider networks and payphones. The company also owns an online contact lens store, OzContacts.com.au, and has at various times in the past had interests in other business lines that have now been exited.

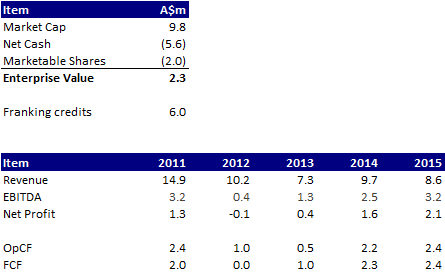

The online contacts business is just break even on an EBITDA basis and not showing particularly fast growth, so I will assume it has no value for the purposes of this analysis. The reverse charge calling services on the other hand is a steady producer of cash flow for the business and has been for some time, allowing the company to build up a significant cash balance (as well as franking credits). The current trading value and recent operating performance of the company is as follows:

As you can see the free cash flow for each of the last two years individually is more than the current enterprise value of the company. However, as can also be seen, the business is in structural decline and this is readily admitted by management and the Board:

While your Board remains committed to the company’s core reverse charge and payphone products, it acknowledges that both areas of operation are under considerable threat from structural industry change. These changes, triggered by the very rapid, global uptake of smartphones, are causing both fixed and mobile telecommunication operators in all markets to radically rethink their business models. The impacts are likely to be profound for the market for reverse charge and payphone services in the long term, but the Board remains confident that the company can continue to operate profitably in these markets in the medium term.

Chairman, 2012 Annual Report

Recognising this, the company started taking steps in FY2012 to exit unprofitable businesses, shut down its international operations and cut costs to manage the profitable Australian businesses for cash. This was exactly the right move and the positive results can be seen in FY2013-2015 as both operating and free cash flow improved significantly. The results were slightly down for the first half of FY2016 (as you would expect), but the business is likely to continue to produce $1-2 million in operating cash flow for at least the next few years.

For a buyer entering at the current valuation, if the cash balance and operating cash flow was returned to shareholders they would likely receive back their initial investment within 1-2 years, and that’s ignoring the substantial value of the franking credits held by the company. However, this is where we start running into the potential value trap issues. Rather than returning the substantial cash balance and ongoing operating cash flows, management decided to invest $2 million in a small minority stake in another listed entity, Onthehouse Holdings (OTH). Quite apart from the business they invested in, which I think is very expensive for what you get (notwithstanding the takeover offer that was forthcoming after the stake was acquired), I am not investing in the company to have management act as a fund manager on my behalf. If I want to take small minority stakes in listed businesses, I can do so myself.

On the face of it, management’s actions appear to be a classic example of the inherent conflict of interest between a management team and the owners of the business. The owners of a business want to see the cash. This is particularly true for dying businesses where the focus should be on maximizing the shrinking cash flow. However, the management team wants to continue getting a salary and will try to revive the dying business or take what cash is available and invest it in other opportunities.

In a best case scenario, the takeover offer that was forthcoming for Onthehouse Holdings after the company purchased its stake will lead to management achieving a profit that can be returned to shareholders. However, it’s a very realistic possibility that the takeover further emboldens them to invest the cash within the business elsewhere. There are not many management teams that can consistently perform M&A well. In fact it is generally a huge destroyer of value for most businesses. All I can say is that if the company makes one more investment similar to Onthehouse Holdings, I’ll be voting with my feet and selling my stock despite the apparent value on offer.