Where Are You Going, Where Have You Been?

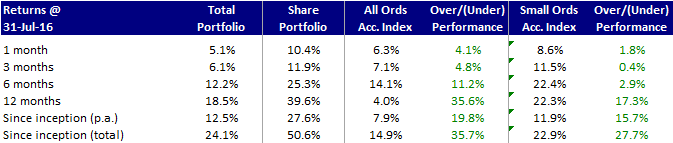

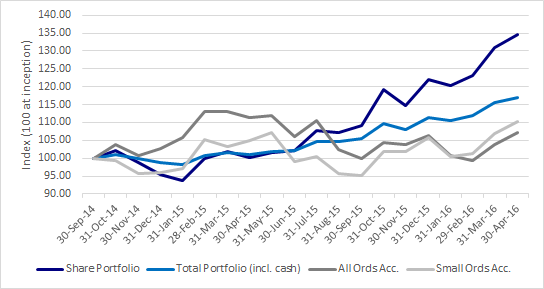

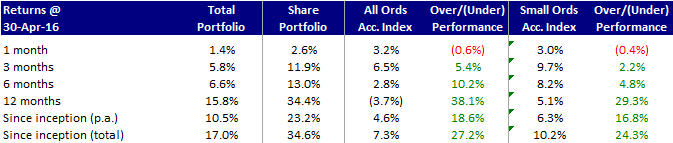

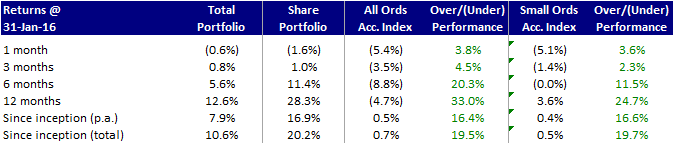

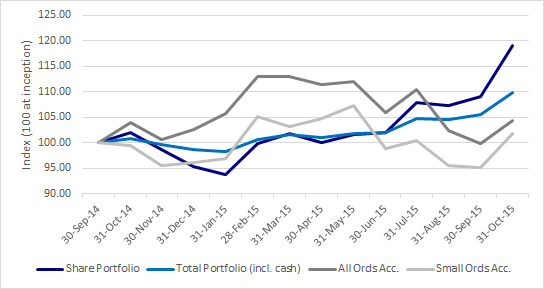

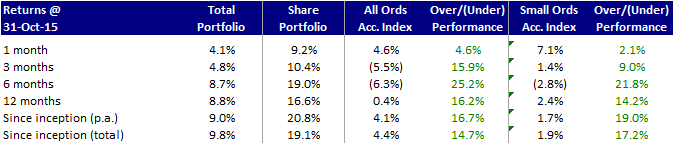

I haven’t written here for what seems like an eternity. The good news is that unlike many people that start a similar blog and then stop because they are performing badly, my portfolio has continued to perform reasonably well. I’ll put up a more detailed performance update soon but the portfolio is up overall and continued to outperform the two comparison indices, although the gains have slowed over the past few months.

The main reason that I took some time out was because I’ve been doing a large amount of research and reading. Since I’m not a full-time investor and have a young family and busy job, it was either the research or the writing and writing took a back seat this time. The main reason I chose a period of research over the writing is the ongoing level of central bank monetary accommodation and extraordinary stimulus programs globally and making sure that I have a better grasp of how this is influencing the markets and what may happen as the various monetary stimulus programs start to unwind. This took me on a pretty winding journey covering topics such as the implementation of the various quantitative easing programs, the fractional reserve banking system, how credit is created in today’s banking system, the various components of the monetary supply, Austrian economics, the gold standard and many more related topics. Amongst all that, I even managed to fit in a reasonable amount of other general reading on investing and behavioural economics.

This was an incredibly interesting period and even though I have a background in finance and banking, I learned a huge amount. I think that many people without a background in finance would be truly amazed at how the banking system functions, the relationship between central and commercial banks and some of the implications of monetary debasement. I’ll pick up on various topics as we move forward but there are two that are worth mentioning now.

Firstly, most of what I uncovered was pretty scary in terms of possible effects on stock markets globally – I was already somewhat worried which is why I am only half invested in the market – and so the question becomes what to do. As I’ve stated previously, I don’t believe in market timing for macro factors. You may get lucky once or twice and hit the top/bottom or hit a major macro event, but all the evidence (both research and anecdotal) suggest that it is almost impossible to do so consistently. Therefore, I don’t want to reduce my exposure any further. I don’t want to short the market because it could continue to go well north of where it is today – in fact often in bull markets the biggest gains come right toward the end. I also don’t have the personal constitution/I’ve settled on a mix of actions:

- I’m periodically purchasing out of the money ASX 200 index puts. This gives you downside protection in a similar way short selling, but unlike shorts you can only lose your initial investment so can control your exposure. In this way, it’s very similar to an insurance policy (i.e., small outlays over time that could result in a big payoff if the market tanks). In addition, I also believe that the pricing is reasonably favourable currently due to suppressed volatility (one of the key inputs to options pricing).

- I have some of my portfolio invested in gold. I fully agree with people that say gold is not a productive asset and I am not including it to serve that purpose (or for short term speculation for that matter). It is being included purely as insurance for (i) general protection from uncertainty (i.e., performs well in down markets), and (ii) also as a hedge against a total meltdown of the current monetary system, which could result in reverting to gold-backed currencies (not as far-fetched as it may seem) – if this occurs I believe that gold could appreciate significantly from it’s current price.

- Ongoing vigilance of the debt levels of companies in my portfolio and companies that I am evaluating. This is a liquidity driven credit market and if that liquidity dries up, I believe that there will be significant dislocation (tightening) of the credit markets, so I want companies with low levels of debt – this was already a strong focus for me, but I’ve stepped up my scrutiny in this regard.

Note that I won’t include either of the put positions and gold purchases (regardless of whether they perform well or not) in the returns analysis on this website as I consider them to be insurance/hedging policies that are separate from my ‘long-only’ investing.

The second thing that I want to note here relates to central bank influence. It is generally accepted that the capitalist system of free markets with open price discovery and signaling (through prices) has generated the fastest growth in living standards, productivity, economic output etc. In particular capitalism has proved to be effective at allocating scarce resources to meet society’s needs. Society’s needs are conveyed through prices – if there is high demand prices go up and encourage further supply and vice versa. Once you lose the informational content contained in prices (e.g. in many communist societies where prices are set centrally), these links break down and resources are not allocated nearly as effectively in terms of meeting society’s needs.

What has been interesting over the past few years in particular is to see many (most) developed capitalist societies start relying on a central banks setting interest rates. Interest rates are simply a price, and so we find ourselves in a position where the price for the most important commodity in existence (money itself) is being set centrally and has lost all signaling value. How far we are from ‘natural’ interest rates is very hard to guess because it is not easily observable unless the market for money ((i.e., interactions between private-sector lenders and borrowers) are functioning freely.

I have no doubt that the central bankers manipulating interest rates through monetary policy genuinely believe that they are doing the right thing. However, it has been shown over and over again throughout history that a few people making decisions generally do a very poor job compared to hundreds of thousands of people interacting through an open market. Some of the results of this are somewhat puzzling. For example, as the debt burden has gone up globally interest rates have been falling rather than rising. This is due to people having the belief that central bankers know what they are doing and will be able to successfully pull off what would be an enourmous balancing act of stimulating the global economy without their monetary policies causing massive price inflation. If people ever lose their faith that the central bankers will be able to accomplish this, then those central bankers will no longer be able to dictate interest rates – rather, the market will tell them that their borrowing cost are actually much higher than the rates that they have been setting, and the whole thing falls apart.

Without getting into big predictions as to whether or when this will happen, I will (for now) simply make the comment that monetary accommodation on the scale that is currently occurring and in so many developed countries/regions at once has never been seen before. At the very least, we need to recognize that this adds a large amount of macro risk (not to mention many of the other effects that artificially low interest rates have) and to try and make sure that we have a plan should it break the wrong way.